Character Change: Why The Markets Refusal to Sell Matters

Weekly Outlook 04/06/26

Market Recap

Coming into the week, markets were carrying oversold conditions from the prior week’s relentless selling. Monday offered no relief, with all-day selling pressure extending the drawdown and keeping the bear case firmly in control.

The turn came Tuesday. Reports circulated that Iran’s president had approached the U.S. about a ceasefire, a claim Trump amplified publicly before Iran’s foreign ministry flatly denied it as “false and baseless.” The brief window was enough to send oil lower, with WTI pulling back toward $100 and Brent dipping briefly below that level as traders priced in a faster resolution to the Strait of Hormuz disruption.

That optimism did not last. Wednesday night, Trump addressed the nation and struck an escalatory tone, vowing to hit Iran harder over the coming weeks with no clear off-ramp provided. Thursday opened with a sharp gap down across indices as crude staged a powerful rally, eventually closing up 11.1% at $111.

What followed was more significant than the gap itself. Buyers stepped in immediately at the open and absorbed supply throughout the session, finishing the day well off the lows. This is the definition of a news failure to the downside: a clean escalation catalyst that the market refused to sell.

Every week in March ended with indices selling off into the weekend. Thursday’s price action was the first meaningful character change since the war began. Stocks closing strong into a long holiday weekend, with participants willingly carrying risk premium through Good Friday, is a notable shift in behaviour.

For the week, the S&P 500 gained 3.4%, the Dow added nearly 3%, and the Nasdaq led with 4.4%. The first weekly gain for all three since the Iran conflict began, and the S&P’s largest weekly rise in four months.

Macro and Jobs

The March nonfarm payrolls print, released Friday while markets were closed for Good Friday, came in at +178,000 against a consensus of +59,000, reversing February’s -133,000. Unemployment edged down to 4.3% and wage growth slowed to 3.5% year-over-year, the lowest since May 2021. Goldman Sachs estimated that weather normalization, resolved strikes, and seasonal adjustments accounted for roughly 122,000 of those gains, softening the headline beat considerably. Fed futures moved to price in a 77.5% probability of rates on hold through year-end, with persistent oil-driven inflation leaving the central bank little room to act.

Watchlist

Before getting into individual names, it is worth flagging some developments over the weekend that could shape the tape materially in the coming weeks. Reports emerged of increased ship traffic through the Strait of Hormuz, with Iraq among the countries declared exempt from restrictions as Iran continues to negotiate arrangements with regional partners.

Additionally, Andreas Steno Larsen published a contrarian piece on X arguing the oil supply shock could be approaching its end within three to four weeks. If that call proves correct, it would be a significant tailwind for equity indices and could mark a top in crude.

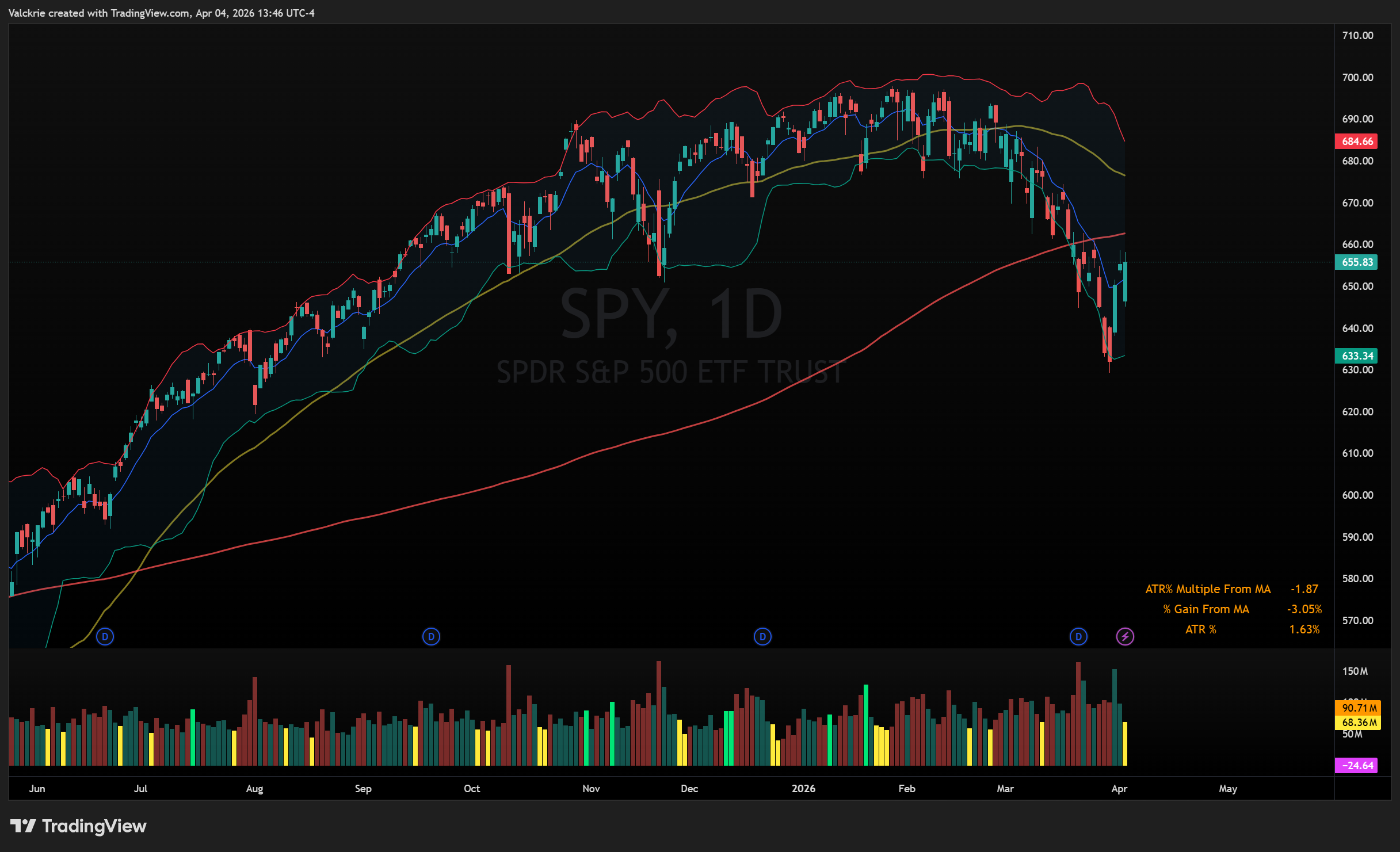

From a technical standpoint, the Thursday and Friday highs from last week are the immediate levels to watch. A break and follow-through above that two-day range would be a constructive signal. $SPY and $QQQ are both within striking distance of reclaiming their 200-day moving averages, while $IWM has been the strongest of the three, having held the 200-day moving average considerably better throughout the drawdown.

The macro backdrop remains news-driven. Beyond the major indices and crude, several stories and sectors are worth tracking into next week.

SpaceX and the Space Sector

The SpaceX IPO trade reignited this week with reports of a valuation increase to $2 trillion. The three publicly traded proxies that hold SpaceX shares directly could offer a swing trade opportunity and run into the IPO event: SATS 0.00%↑ DXYZ 0.00%↑ and NASA 0.00%↑.

More broadly, the space sector has remained one of the stronger pockets of the market. The ETFs UFO 0.00%↑, ARKX 0.00%↑, ITA 0.00%↑, and XAR 0.00%↑ reflect that relative strength at the index level.

Within the space stock basket, names worth tracking include RKLB 0.00%↑ LUNR 0.00%↑ PL 0.00%↑ FLY 0.00%↑ ASTS 0.00%↑ RDW 0.00%↑ SATS 0.00%↑ SATL 0.00%↑ GSAT 0.00%↑ VOYG 0.00%↑ BKSY 0.00%↑ FJET 0.00%↑ SIDU 0.00%↑ YSS 0.00%↑ SPCE 0.00%↑.

Fresh IPOs

SWMR 0.00%↑ is a recent drone IPO that closed above its IPO highs this week. A stock printing strength above its IPO price in a difficult tape is worth monitoring for further momentum.

Private Credit

OWL 0.00%↑ received negative news Friday around further redemptions in two of its major private credit funds, though it closed well off the lows. Worth watching to see how it digests that news into next week.

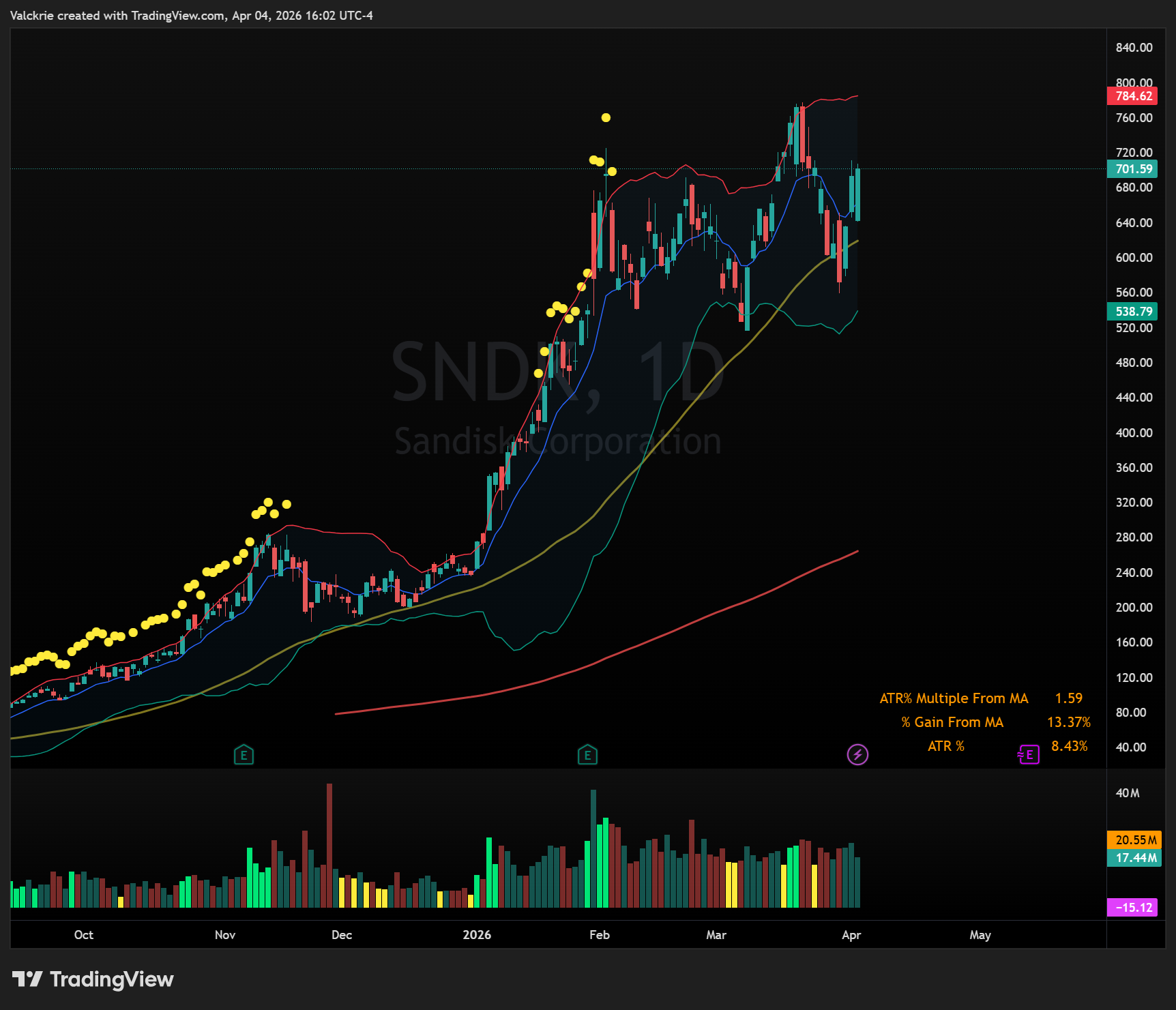

Memory

Memory stocks held up well throughout the latest market pullback, showing relative strength when most of the market was under pressure. SNDK 0.00%↑ WDC 0.00%↑ and STX 0.00%↑ remain on watch.

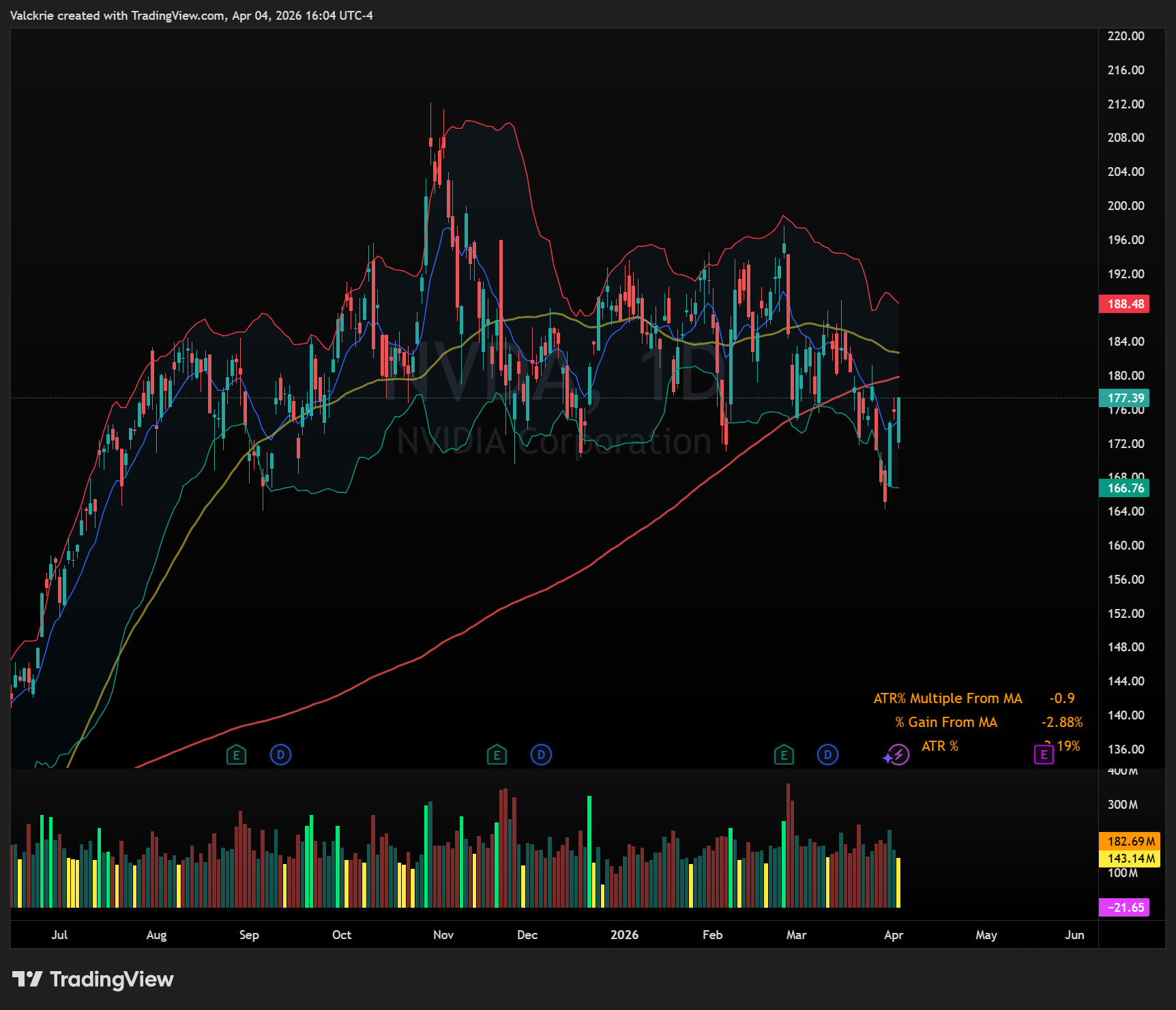

Semiconductors

The preferred focus within semis is on names that remain in uptrends and have held their technical structure. INTC 0.00%↑ and AMD 0.00%↑ both held the 200-day moving average and stayed within their base consolidation ranges during the market drawdown.

ARM 0.00%↑ had a notable catalyst two weeks ago with the announcement of a new chip product and entry into the GPU market. TSEM 0.00%↑ also strong but may have already provided their best entry points given the breakout on Thursday.

NVDA 0.00%↑ remains less attractive by comparison, having broken down from its multi-month trading range and still sitting below the 200-day moving average, technically in a brief downtrend still.

TSLA 0.00%↑ reported Q1 deliveries and production rose year-over-year but fell from the prior quarter. More notably, it was visibly weak on Thursday, closing near the lows of the session on a day when the broader market was finishing near highs. That divergence is worth noting.

Photonic Computing

Photonic computing stocks have been among the strongest groups in the market and largely remained in uptrends throughout the recent market downdraft, holding above key moving averages. LITE 0.00%↑, GLW 0.00%↑, COHR 0.00%↑, and AAOI 0.00%↑ are the names to track here. Setups are not yet fully actionable across the group, but the relative strength warrants keeping them on the radar.

Closing Thoughts

The weight of evidence this week tilted toward the bulls for the first time since the conflict began. Oversold conditions, a news failure to the downside, a strong close into a long weekend, and early signs of a potential resolution in the Strait all point in the same direction. That does not mean the all-clear has been sounded. The tape remains headline-driven and crude remains the variable that everything else trades around. But the character of price action shifted this week, and that is worth respecting. The levels are clear, the catalysts are in view, and the market has shown it is willing to buy. How it handles the follow-through next week will tell us a great deal about whether this is a genuine turn or simply a relief rally in a still-broken trend.

Weekly recaps only tell part of the story. For daily market coverage, live commentary at the open, real-time trade ideas, and watchlists, join the Discord community below.