From Viral Substack to War: AI Panic Meets Geopolitical Reality

Weekly Outlook 03/02/26

Market Recap

The Citrini Selloff

Markets gapped down hard on Monday after Citrini Research’s “The 2028 Global Intelligence Crisis” went viral over the weekend. The 5,000-word thought experiment, written as a fictional dispatch from June 2028, painted a scenario where aggressive AI adoption hollows out white-collar employment, crushes consumer spending, and ultimately crashes the S&P 500 38% from hypothetical October 2026 highs. Michael Burry amplified it on X with the caption: “And you think I’m bearish.” The post racked up roughly 28 million views at the time of writing.

The damage was immediate. Enterprise software stocks bore the brunt, with IGV hitting new 52-week lows, falling around 5% on Monday alone and extending its brutal 2026 decline to nearly -30% YTD. Financials and services companies named in the piece also took collateral damage, as markets priced in the second-order implications of AI-driven disruption to lending, insurance, and intermediation businesses.

Software Bounce

After the Monday washout, software staged a relief bounce through the rest of the week. Anthropic’s enterprise showcase on Tuesday, highlighting partnerships with Salesforce and other major software vendors, helped ease the panic. IGV recovered roughly +2% on Tuesday as investors reconsidered whether the AI threat to software had been overpriced in a single session. The bounce carried into Wednesday and Thursday, though it was modest relative to the damage already done. By Friday the sector gave back some ground again, and the broader question of whether software’s -30% YTD decline represents a buying opportunity or a structural re-rating remains very much open.

NVDA Earnings: Beat, But Still Stuck

Nvidia was the main event of the week. Tech rallied optimistically into Wednesday’s after-hours report, and NVDA 0.00%↑ delivered on virtually every metric. Q4 revenue came in at $68.1 billion, up 73% year-over-year, beating consensus by roughly $2 billion. Data center revenue hit $62.3 billion, up 75% YoY. EPS of $1.62 topped the $1.53 estimate. Gross margins recovered to 75.2%, ahead of guidance. And the Q1 FY27 outlook of $78 billion blew past the $72.6 billion Street estimate.

All of that, and the stock still could not break out of the sideways range it has been trading in since its all-time high of $212 back in October 2025. NVDA popped initially after hours, rising about 3.5%, then gave most of it back. By Friday’s close it had actually sold off to $177, roughly 4% lower on the day and well below where it started the week. For a stock printing 73% revenue growth with accelerating guidance, the inability to sustain upside tells you something about the positioning and expectations already baked in.

SMH also flashed a false breakout, briefly tagging new highs around $427 before fading sharply into the end of the week. The 52-week range now reads $170 to $428, and that mid-week rejection at resistance is worth noting for anyone watching semis closely.

Crypto

Crypto remained range-bound. Bitcoin hovered around $65,000-$67,000 for most of the week, taking directional cues from risk sentiment rather than any crypto-specific catalyst. The weekend Iran escalation pressured BTC briefly below $65,000 before a partial recovery.

Korea: Parabolic Territory

South Korea’s KOSPI was one of the biggest stories of the week and continues to be a top watch heading into March. The index crossed 6,000 for the first time on Wednesday, surging past the milestone just 34 days after breaching 5,000, the fastest 1,000-point advance in its history. By Thursday, post-NVDA euphoria pushed KOSPI to a record close of 6,307, a 3.67% single-day gain driven by Samsung Electronics and SK Hynix, which together now account for roughly 40% of total KOSPI market cap.

The index is up over 47% YTD and has climbed 175% from its April 2025 trough, powered by the memory-chip supercycle and HBM demand from AI infrastructure buildout. Governance reforms under President Lee Jae-myung have also helped close the long-standing “Korea discount,” drawing foreign and domestic capital back into the market.

On Friday, the KOSPI pulled back about 1% as global funds sold a record 6.8 trillion won ($4.7 billion) in a single session of profit-taking. But the index still held above 6,200, recovering reasonably well. The intraday pullback was notable but not destructive.

This remains a top watch in the coming weeks. Parabolic moves like this tend to produce the highest volatility near the peaks, and the concentration risk in Samsung and SK Hynix is extreme. Any disruption to the memory cycle or a shift in HBM demand expectations could trigger a sharp correction. Keep it on the radar.

Metals and Oil: War Premium Builds Into the Close

Heading into Friday, metals started to get bid. Gold and silver both made notable moves higher as the market began front-running potential weekend escalation involving Iran. Crude oil also firmed, closing at $67.02, up nearly 3% on the day. The positioning felt deliberate, with commodities traders pricing in geopolitical risk ahead of the weekend.

That risk materialized in full. On Saturday, the US and Israel launched a massive joint military operation against Iran. Airstrikes targeted leadership compounds, military installations, and strategic sites across Tehran and other cities. Iranian state media confirmed early Sunday that Supreme Leader Ayatollah Ali Khamenei had been killed in the strikes, along with the country’s defense minister, the IRGC commander, and several other top officials.

Iran responded with retaliatory missile and drone strikes against Israel, the UAE, Qatar, Kuwait, Bahrain, and Saudi Arabia, hitting US bases in the region and spreading the conflict across the Gulf.

As of Sunday’s futures open:

Brent crude jumped roughly 11% opening at ~$75/barrel

Gold rose ~1.6%, trading above $5,300/oz, extending its seventh straight monthly gain

S&P 500 futures dropped nearly 1%

Nasdaq 100 futures fell ~1.2%

Watchlist

Given the scale of this weekend’s geopolitical shock and the uncertainty still unfolding in the Middle East, this could easily be a macro-driven week where individual stock catalysts take a backseat to headline risk. $VIX nd VXX 0.00%↑ will be the first things to watch at Monday’s open as the market reprices volatility around a live military conflict and the Strait of Hormuz situation. The major indices (SPY, QQQ, DIA) will set the tone early.

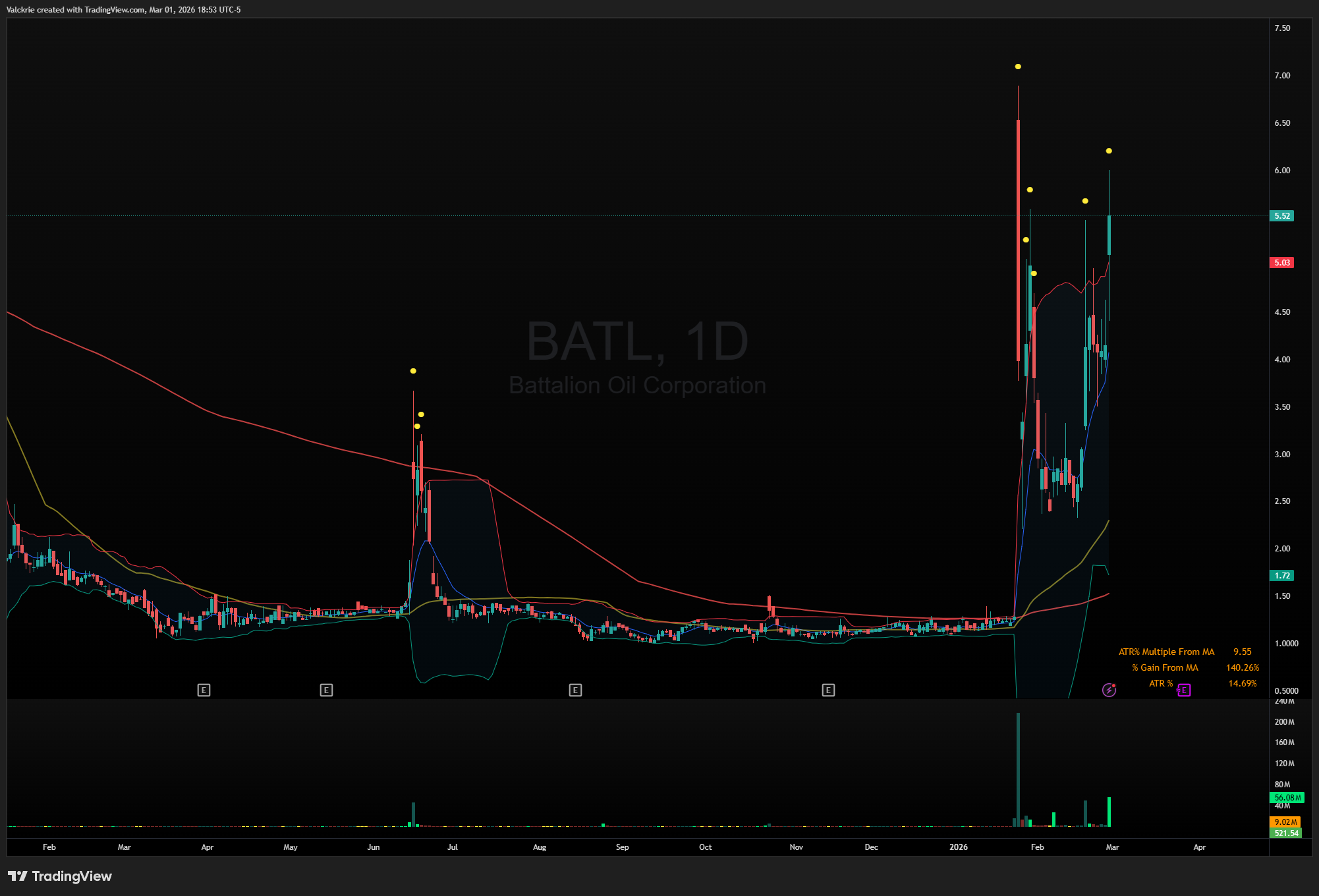

Oil, silver, and gold will be in play all week. Brent crude is already up 10% on the Sunday open, gold is trading above $5,300, and silver is pressing toward $95. If the Strait of Hormuz remains disrupted, these moves have room to run significantly further. Watch for momentum in small and microcap oil names: BATL 0.00%↑, INDO 0.00%↑.

Defense and drone stocks could also find a bid as the market processes the implications of an active US military campaign. PRZO 0.00%↑ UMAC 0.00%↑ UAVS 0.00%↑ KTOS 0.00%↑ RCAT 0.00%↑ ONDS 0.00%↑ DPRO 0.00%↑.

NVDA 0.00%↑ remains on watch after selling off post-earnings despite beating on every metric. The stock dropped to $177 by Friday’s close, well below its mid-week highs, and has now spent over four months unable to break out of the $170-$210 range.

MU 0.00%↑ and SNDK 0.00%↑ trade in correlation with the Korea story. With the KOSPI up 47% YTD and Samsung/SK Hynix driving the memory supercycle, any continuation or sharp reversal in Korean equities will likely pull these names along with it.

NFLX 0.00%↑ after walking away from the WBD merger on Thursday. Paramount Skydance’s $31/share bid was deemed a “superior proposal,” Netflix declined to match, and collected a $2.8 billion termination fee for its trouble. The stock closed up over 13% on the day on relief that the deal is dead.

XYZ 0.00%↑ (Block) after Jack Dorsey cut nearly half the workforce, laying off 4,000 employees, and directly attributed the decision to AI efficiency gains. Dorsey predicted most companies will make similar structural changes within the next year. This is both a company-specific catalyst and a broader signal for the AI-displacement theme that has been weighing on software and services all year.

Space names are in focus after Bloomberg reported Friday that SpaceX is preparing to file confidentially for an IPO as soon as March, targeting a valuation above $1.75 trillion. If that filing materializes, it should provide a valuation anchor for the entire space sector. SATS 0.00%↑, DXYZ 0.00%↑, RKLB 0.00%↑ all trade as public proxies for SpaceX exposure and could see increased flows.

Quantum stocks sold off after earnings this week, with QBTS 0.00%↑ threatening to make new lows.

Weekly recaps only tell part of the story. For daily market coverage, live commentary at the open, real-time trade ideas, and watchlists, join the Discord community below.