Oil in Crisis, Korea Reverses, and the VIX Wakes Up

Weekly Outlook 03/09/26

Market Recap

It was a week that delivered volatility in spades, with multiple macro shocks colliding across equities, commodities, and global markets simultaneously.

Korea’s Parabolic Run Hits a Wall

The South Korea ETF’s EWY 0.00%↑ extraordinary run, which had been one of the standout global stories over the past several weeks, finally reversed course this week. Parabolic moves rarely end gracefully, and this one was no exception. After weeks of relentless buying fueled by AI-driven demand for semiconductors and memory, the index ran out of buyers. The reversal serves as a reminder that even the strongest trends need to breathe, and that chasing price at extended levels carries real risk.

Oil Takes Center Stage

The dominant story of the week was oil, after Saturday’s significant attack on Iranian energy infrastructure sent shockwaves through commodity markets. Oil had already been tracking higher into the event, but the weekend news turned an already-tense setup into a full-blown supply shock narrative. Oil continued to rise every day throughout the week, culminating into Sunday’s futures open, which saw crude gapping up close to 20%, one of the more violent overnight moves in recent memory.

The Strait of Hormuz, the critical chokepoint through which a meaningful share of global oil supply flows, is now effectively deadlocked. No oil is moving through. The severity of the disruption is drawing comparisons to some of the worst supply shock episodes of the past decade, and by most assessments this situation ranks among the more serious ones we have seen.

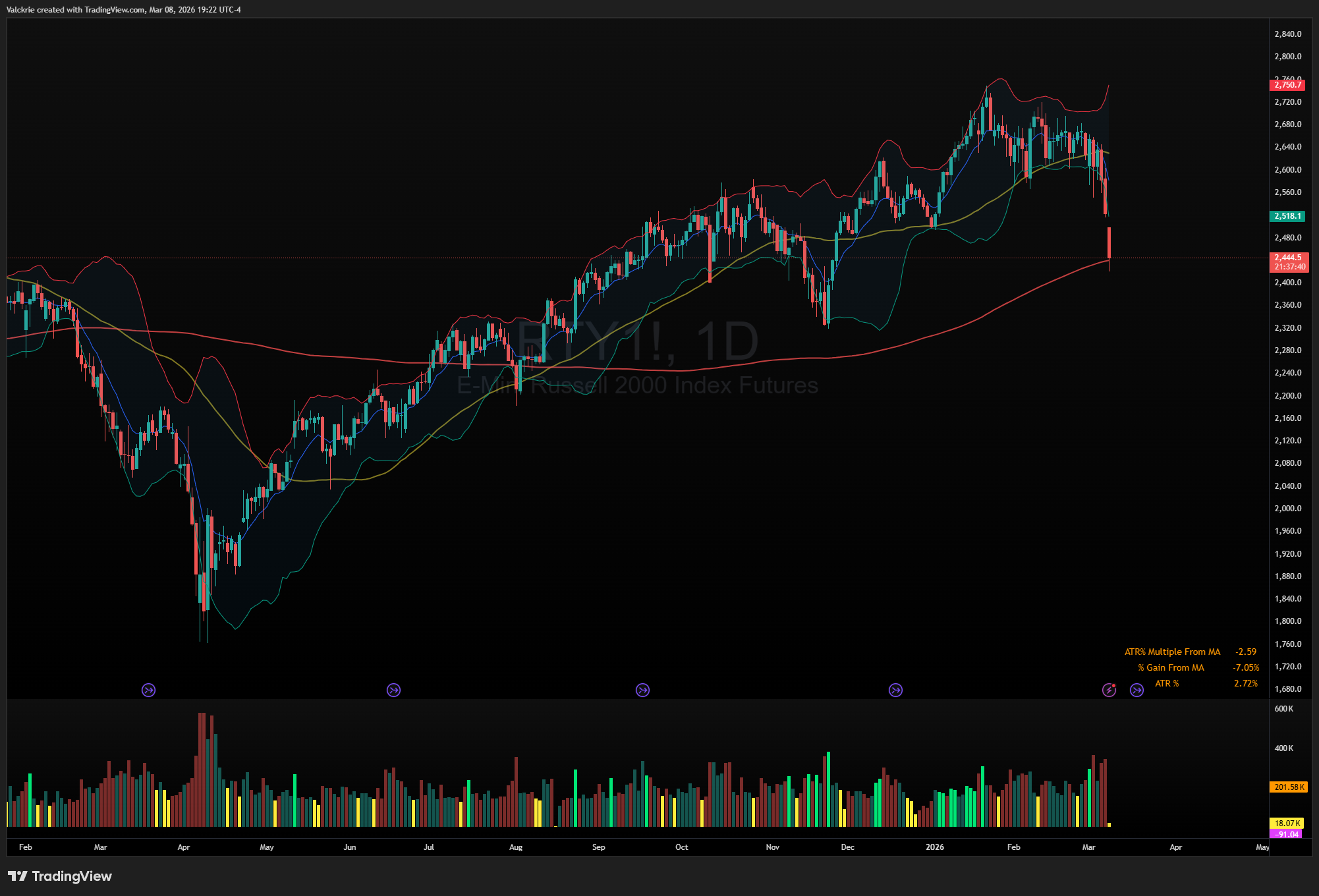

Equity index futures also opened sharply lower on Sunday open to kick off the week. The Russell 2000 futures was down approximately 4% at the open, with small caps bearing the brunt of the selling given their sensitivity to energy costs and domestic economic conditions.

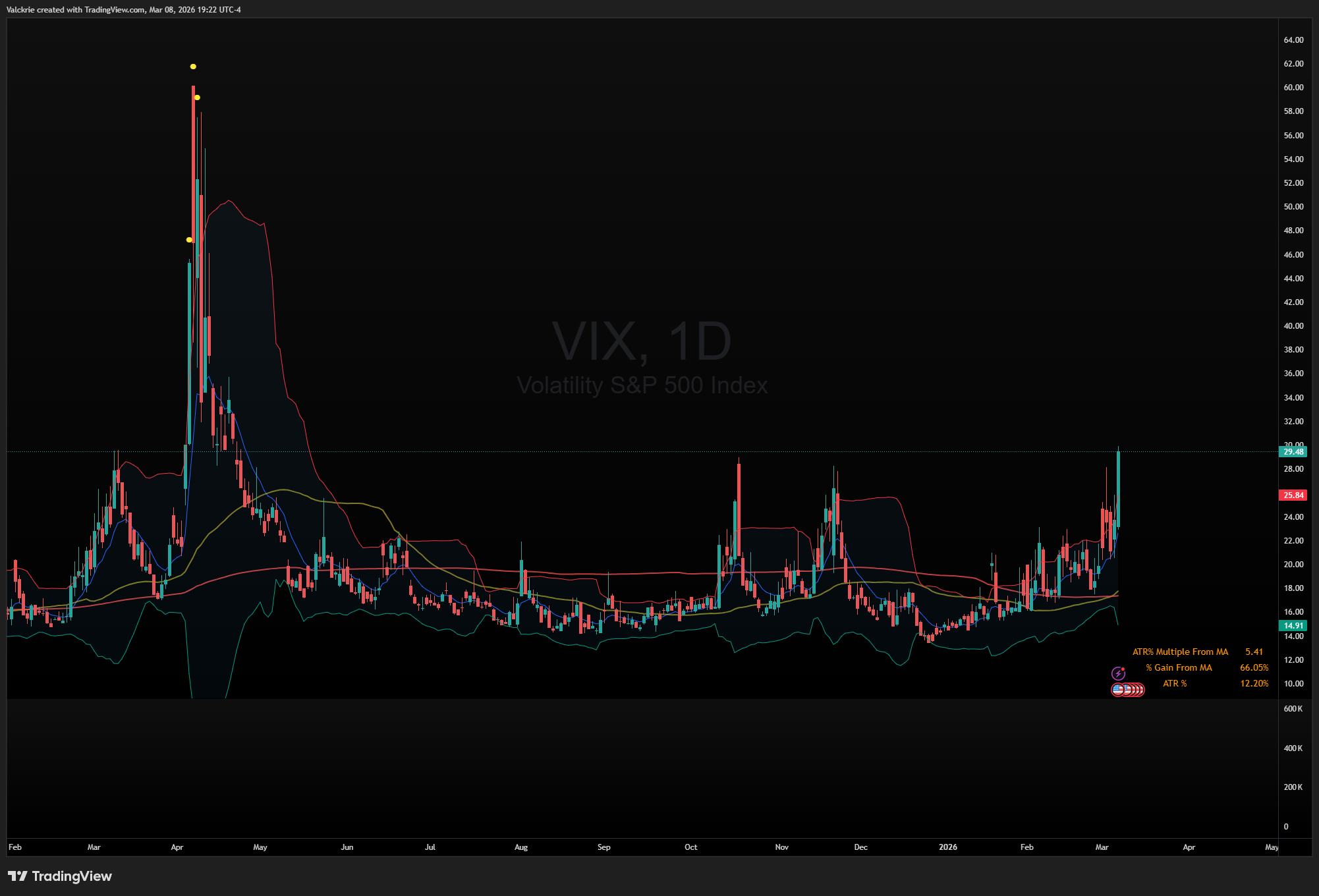

VIX Breaks Out, SPY and QQQ in a Vulnerable Spot

Fear is back. The VIX broke out meaningfully this week, confirming that traders are no longer willing to dismiss the macro risks building in the background. Both SPY 0.00%↑ and QQQ 0.00%↑ are now sitting in technically vulnerable positions. The indices had been holding above key moving averages through the earlier chop, but the combination of an oil shock, a VIX breakout, and deteriorating risk appetite has put those levels in jeopardy.

Watchlist

It will be a volatile, macro-driven week. Iran and geopolitical headlines remain the primary variable to monitor. Any meaningful reversal in oil will likely require either a clear de-escalation or a fundamental shift in the Hormuz situation. Until that happens, expect oil to remain elevated and reactive to every headline.

Oil and Energy

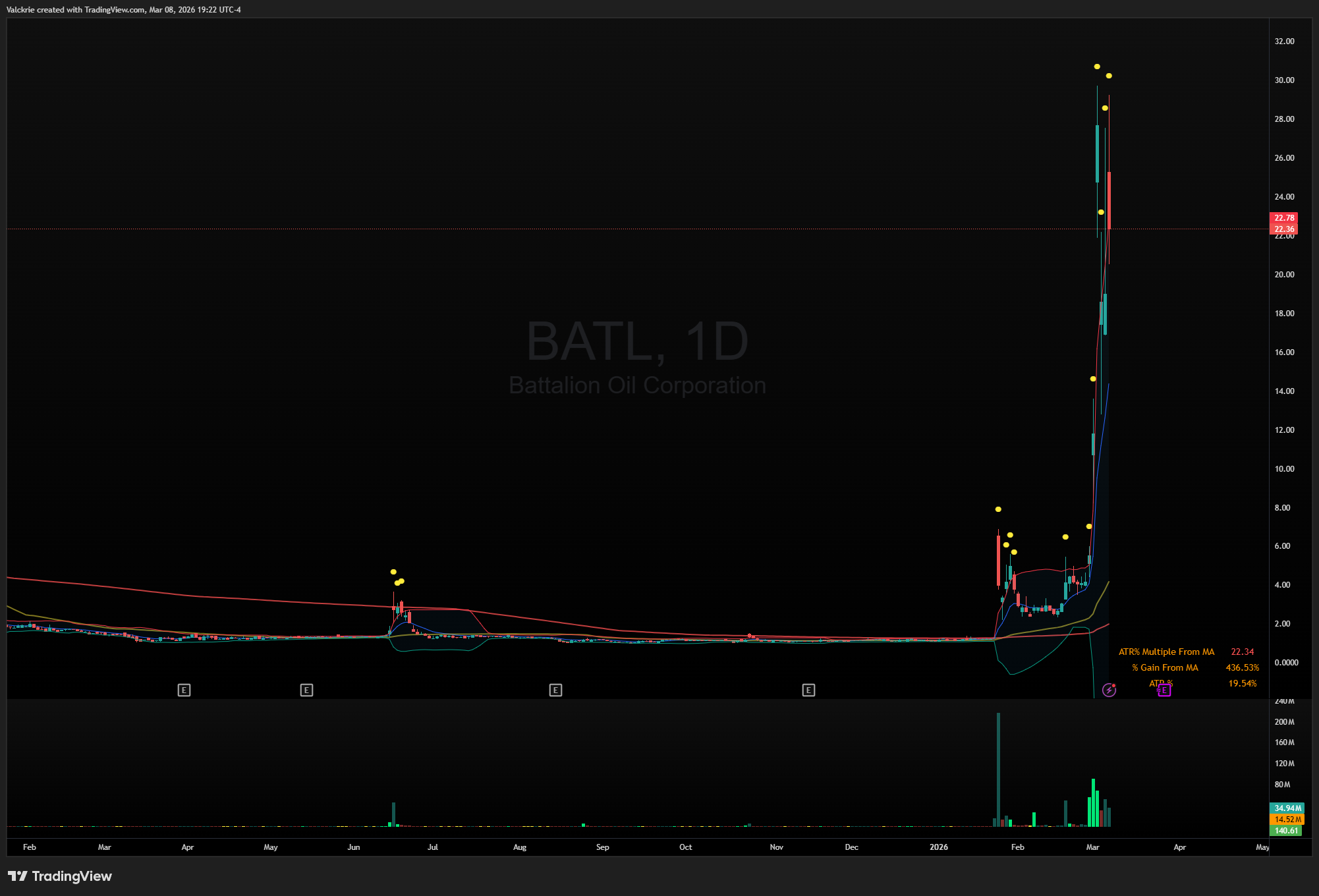

CL and USO 0.00%↑ are the obvious vehicles to watch. The oil microcap names that were in play last week, BATL 0.00%↑ , TMDE 0.00%↑, and TPET 0.00%↑, will continue to see elevated volatility and wide trading ranges. These are not set-and-forget trades. They move fast in both directions and need to be managed accordingly.

Semiconductors and Memory

SNDK 0.00%↑ and MU 0.00%↑, two names that had been holding up relatively well as market leaders, finally started to roll over this week under the weight of broader market weakness. Both are now trading below short-term moving averages, which shifts the near-term bias. Worth watching to see if they reclaim those levels or continue to deteriorate.

Drone Stocks

RCAT 0.00%↑ and ONDS 0.00%↑ both had sharp rallies earlier in the week but gave back the majority of their gains, formin a bearish wick. Depending on further market weakness could be vehicles to join on the short side.

Earnings

MRVL 0.00%↑ and IOT 0.00%↑ both had strong post-earnings reactions this week, a positive signal in an otherwise difficult tape. Earnings-driven strength in a down market tends to stand out.

HIMS and NVO

Late Friday, Bloomberg reported that Novo Nordisk and Hims & Hers have resolved their legal dispute and are preparing to announce a new partnership to sell Wegovy on the Hims platform, with the announcement expected as early as Monday. HIMS 0.00%↑ surged nearly 40% in after-hours trading, trending as the top name on Stocktwits, while NVO 0.00%↑ gained around 2%. The backstory here is a long and bitter one. The two companies had a similar arrangement last year, but Novo scrapped it after Hims refused to stop marketing compounded versions of the drugs. This time around the settlement comes with the expectation of stricter compliance with FDA-approved formulations. A significant catalyst for both names heading into the open on Monday.

SPY Additions

Friday also brought news that VRT 0.00%↑, COHR 0.00%↑, and LITE 0.00%↑ are being added to the S&P 500. Index inclusion events tend to drive mechanical buying pressure in the near term and are worth monitoring as the additions are implemented.

Weekly recaps only tell part of the story. For daily market coverage, live commentary at the open, real-time trade ideas, and watchlists, join the Discord community below.